Portfolio Allocation#

In this quick tutorial, the portfolio allocation problem will be investigated. Of course, this is not financial advice in any way but should illustrate how multi-objective optimization can be applied to a quite interesting problem.

Let’s start by loading some data for illustration purposes. Feel free to use your own.

[1]:

import pandas as pd

import numpy as np

from pymoo.util.remote import Remote

file = Remote.get_instance().load("examples", "portfolio_allocation.csv", to=None)

df = pd.read_csv(file, parse_dates=True, index_col="date")

This tutorial is based on the Markowitz Mean-Variance Portfolio Theory and thus, we need to calculate the mean returns and covariances:

Info

Note that the problem in this case study can be solved directly using a quadratic solver (which will be much more efficient). However, such a solver finds only a single solution and must run multiple times to approximate the Pareto-optimal front. Moreover, it is worth noting that if we slightly change the problem to cubic or non-polynomial, it can not be applied anymore. The method shown provides more flexibility, for instance, optimizing objectives derived from Monte-Carlo sampling.

[2]:

returns = df.pct_change().dropna(how="all")

mu = (1 + returns).prod() ** (252 / returns.count()) - 1

cov = returns.cov() * 252

mu, cov = mu.to_numpy(), cov.to_numpy()

labels = df.columns

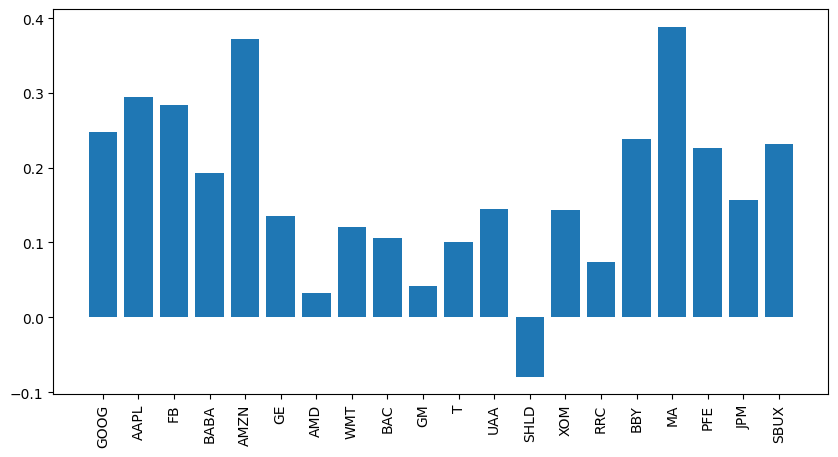

import matplotlib.pyplot as plt

fig, ax = plt.subplots(figsize=(10, 5))

k = np.arange(len(mu))

ax.bar(k, mu)

ax.set_xticks(k, labels, rotation = 90)

plt.show()

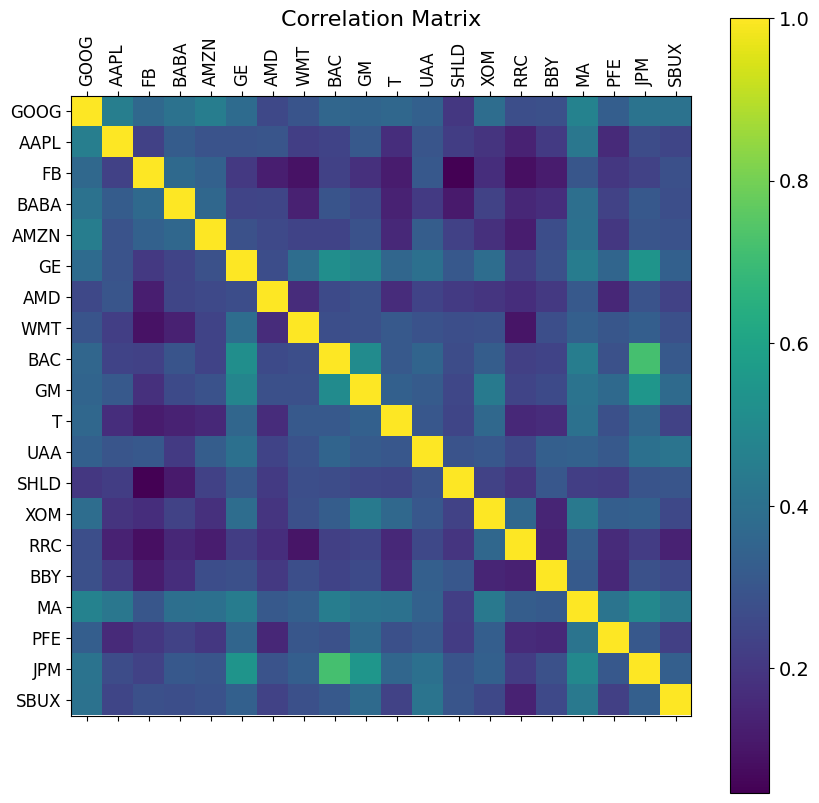

f = plt.figure(figsize=(10, 10))

plt.matshow(returns.corr(), fignum=f.number)

plt.xticks(k, labels, fontsize=12, rotation=90)

plt.yticks(k, labels, fontsize=12)

cb = plt.colorbar()

cb.ax.tick_params(labelsize=14)

plt.title('Correlation Matrix', fontsize=16)

print("DONE")

DONE

Then let us define an optimization problem based on the theory mentioned above:

[3]:

from pymoo.core.problem import ElementwiseProblem

class PortfolioProblem(ElementwiseProblem):

def __init__(self, mu, cov, risk_free_rate=0.02, **kwargs):

super().__init__(n_var=len(df.columns), n_obj=2, xl=0.0, xu=1.0, **kwargs)

self.mu = mu

self.cov = cov

self.risk_free_rate = risk_free_rate

def _evaluate(self, x, out, *args, **kwargs):

exp_return = x @ self.mu

exp_risk = np.sqrt(x.T @ self.cov @ x)

sharpe = (exp_return - self.risk_free_rate) / exp_risk

out["F"] = [exp_risk, -exp_return]

out["sharpe"] = sharpe

Now, we should consider one more fact. The variable x defines what percentage we will invest in what product. Thus, it can not be more than 100% in total. Moreover, an investment of a very small fraction does not really make sense. Thus we also incorporate each weight to be at least 1e-3 of the overall investment.

To ensure both, we can use a Repair operator (also see here) which will be directly used by the optimization method.

[4]:

from pymoo.core.repair import Repair

class PortfolioRepair(Repair):

def _do(self, problem, X, **kwargs):

X[X < 1e-3] = 0

return X / X.sum(axis=1, keepdims=True)

Now let’s see what solutions are found to be optimal:

[5]:

from pymoo.algorithms.moo.sms import SMSEMOA

from pymoo.optimize import minimize

problem = PortfolioProblem(mu, cov)

algorithm = SMSEMOA(repair=PortfolioRepair())

res = minimize(problem,

algorithm,

seed=1,

verbose=False)

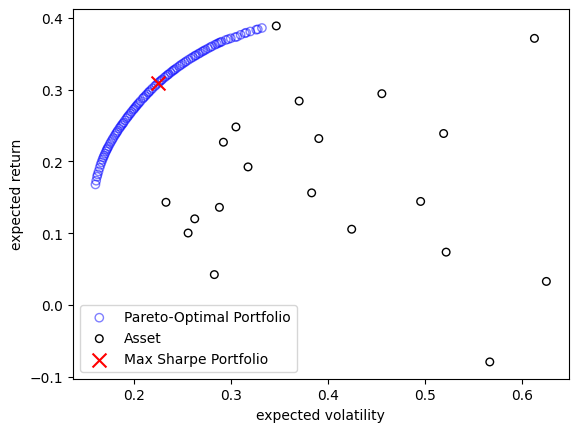

The algorithm has obtained a Pareto-optimal set trading off the mean return and volatility of the portfolio.

[6]:

X, F, sharpe = res.opt.get("X", "F", "sharpe")

F = F * [1, -1]

max_sharpe = sharpe.argmax()

plt.scatter(F[:, 0], F[:, 1], facecolor="none", edgecolors="blue", alpha=0.5, label="Pareto-Optimal Portfolio")

plt.scatter(cov.diagonal() ** 0.5, mu, facecolor="none", edgecolors="black", s=30, label="Asset")

plt.scatter(F[max_sharpe, 0], F[max_sharpe, 1], marker="x", s=100, color="red", label="Max Sharpe Portfolio")

plt.legend()

plt.xlabel("expected volatility")

plt.ylabel("expected return")

plt.show()

A common way for decision making is looking at the sharpe ratio shown below:

[7]:

import operator

allocation = {name: w for name, w in zip(df.columns, X[max_sharpe])}

allocation = sorted(allocation.items(), key=operator.itemgetter(1), reverse=True)

print("Allocation With Best Sharpe")

for name, w in allocation:

print(f"{name:<5} {w}")

Allocation With Best Sharpe

MA 0.34936403519983833

FB 0.203827821244844

PFE 0.2007374998799269

BABA 0.07815268746995567

AAPL 0.06618724520463111

AMZN 0.0352260920851464

GOOG 0.03378174545785696

SBUX 0.018771469602614495

BBY 0.013951403855186296

GE 0.0

AMD 0.0

WMT 0.0

BAC 0.0

GM 0.0

T 0.0

UAA 0.0

SHLD 0.0

XOM 0.0

RRC 0.0

JPM 0.0